TrendForce Just Doubled Its Memory Pricing Forecast. Data Credit: TrendForce.

For IT procurement officers and data center managers, the start of 2026 has felt less like a new fiscal year and more like a high-stakes auction. If you were hoping for the “inventory normalization” many analysts predicted late last year, the latest data suggests a much harsher reality. We are currently witnessing a historic “seller’s market” where the cost of entry is rising faster than most budgets can be revised.

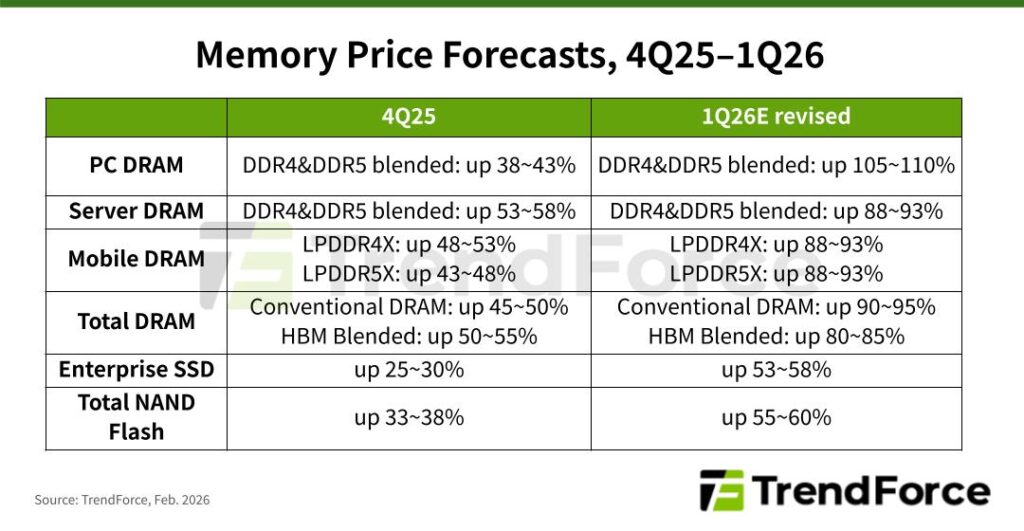

On February 2, 2026, TrendForce issued a radical upward revision to its Q1 pricing expectations. The sheer scale of this adjustment is unprecedented, signaling that the AI-driven memory shortage has moved from a temporary bottleneck to a structural “supercycle.”

The Radical Revision: Breaking Down the Numbers

The initial January forecasts were already aggressive, but they failed to capture the intensity of the demand spike from North American Cloud Service Providers (CSPs) and the aggressive supply-side pivot toward High Bandwidth Memory (HBM).

According to the updated TrendForce report, the firm has essentially doubled its price hike estimates across every major category. The “blended” price increases are no longer just incremental; they are hitting record highs for a single-quarter jump:

-

PC DRAM: Projected to increase by over 100% QoQ, setting a new historical record (contract pricing — quarterly OEM supply agreements that determine system BOM costs, not spot or retail DIMM prices; this pricing basis applies to all figures below).

-

Conventional DRAM: Revised from a 55–60% increase to a staggering 90–95% QoQ jump.

-

Server DRAM: Projected to rise by approximately 88–93%, driven by intense competition among server OEMs.

-

Enterprise SSDs: Forecasted to climb by 53–58% as AI inference demand outstrips production capacity.

-

NAND Flash: Revised from 33–38% to 55–60% QoQ.

Strategic Warning: These figures are not just abstract market data. For an organization planning a 1,000-unit server refresh, a 90% jump in DRAM costs can translate into millions of dollars in unbudgeted capital expenditure, potentially stalling digital transformation projects across the enterprise.

Why the Forecast Shifted So Violently: The $650 Billion Race

The primary reason for this sudden price explosion isn’t just a supply shortage—it is an unprecedented “capex war” among the world’s largest technology firms. For 2026, the big four hyperscalers—Amazon, Google, Meta, and Microsoft—have signaled a collective capital expenditure plan of roughly $650 billion.

This spending is focused almost entirely on AI infrastructure, with Amazon alone planning to spend $200 billion by the end of the year. This flood of capital is effectively “locking up” the global supply of high-end silicon, leaving traditional enterprise and consumer sectors to fight for the remaining scraps.

The HBM4 “Wafer Penalty”: A Death Knell for Low Prices

As of February 16, 2026, the memory market has officially transitioned from “anticipation” to “aggressive execution.” We are no longer talking about samples or pilot runs; the world’s three largest memory manufacturers have fully pivoted their foundries to HBM4 to feed NVIDIA’s insatiable demand. This massive, coordinated shift is the primary engine driving up the cost of every other type of memory and storage on the market.

The State of Play: Mass Production is Now Live

The “Big Three” have hit critical milestones in just the last 96 hours, signaling a total commitment to the HBM4 era:

-

Samsung: On February 12, 2026, Samsung announced it has begun mass production and commercial shipments of the industry’s first HBM4. Utilizing its 6th-generation 10nm-class (1c) DRAM process, Samsung’s HBM4 delivers a blistering 11.7 Gbps processing speed, specifically optimized for NVIDIA’s upcoming Vera Rubin architecture.

-

Micron: Just one day earlier, on February 11, 2026, Micron confirmed it has also entered volume production and started shipping HBM4. Micron’s stock surged 10% on the news that its 2026 supply is already 100% sold out, with its chips meeting the rigorous pin-speed requirements for next-gen AI accelerators.

-

SK Hynix: The market leader has kickstarted full-scale HBM4 production at its flagship M16 plant in Icheon and the new M15X fab. By partnering with TSMC for the logic base die, SK Hynix is currently delivering the high-density 12-layer stacks required for the NVIDIA Rubin platform, which is itself in full production as of Q1 2026.

This focus on HBM4 creates a “Wafer Penalty.” Because HBM4 is physically larger and more complex, producing a single HBM wafer displaces the capacity of approximately three conventional DRAM wafers. Furthermore, current HBM4 yields hover around 50%, compared to 70% for standard DDR5. Every wafer dedicated to HBM is a wafer taken away from the server and PC DRAM markets, leading to the staggering price hikes we see today.

Real-World Evidence: The Price of “Wait and See”

We are already seeing these predictions manifest in the spot market and contract negotiations. The days of affordable high-capacity storage have vanished almost overnight.

-

The Server Memory Surge: The contract price for a standard 64GB RDIMM module has reportedly jumped from $450 in Q4 2025 to over $900 in Q1 2026, effectively doubling in 90 days.

- Storage Inflation: High-capacity 30TB enterprise SSDs that were $3,000 last year are now approaching **$11,000 per unit**.

-

NAND Inventory Depletion: Phison CEO Khein-Seng Pua recently confirmed that all 2026 NAND production capacity is already sold out, with the cost of a 1TB TLC chip surging from $4.80 to over $10.70.

-

BOM Inflation: In the smartphone sector, memory once accounted for 10-15% of total production costs; that figure has now surged to 30-40%, forcing brands like Xiaomi and Dell to prepare for significant retail price hikes later this year.

Strategic Implications: Converting Volatility into Financial Leverage

The current memory supercycle should not be viewed solely as a procurement crisis. It represents a broader capital allocation challenge affecting enterprises, cloud-native startups, research institutions, and system integrators alike. When DRAM and NAND pricing surges within a single quarter, traditional refresh cycles and fixed-budget planning models become structurally misaligned with market reality.

Elevated component costs also increase the economic value of existing infrastructure. As replacement costs rise, the embedded memory and storage inside deployed servers and storage arrays become more financially significant. This dynamic temporarily transforms hardware from a predictable depreciating asset into a variable-value capital resource. For organizations evaluating whether to sell server RAM, or sell SSD, the current pricing environment may represent a peak liquidity window rather than a routine disposal cycle.

Organizations navigating this environment should focus on two parallel priorities:

-

Maximizing utilization efficiency to delay unnecessary expansion

-

Assessing whether surplus DDR4, DDR5, or enterprise SSD inventory can be strategically monetized

In a hyperscaler-dominated supply environment, memory and storage behave less like commodities and more like constrained strategic inputs. Enterprises that treat infrastructure as a flexible financial asset—rather than a fixed operational expense—will be better positioned to withstand continued volatility throughout the AI-driven semiconductor cycle.